G is for...Google

Organising the world's information and re-organising media agencies for the better

They say there’s only two ways to make money in the world.

Bundling and unbundling.

In the late 90s savvy leaders of what used to be media departments within advertising agencies, figured out that they could create more value for clients, and make more money for shareholders, if they unbundled media services from full-service advertising agencies.

By going solo not only could they handle the media buying for their original parents, but they could also pitch for clients of other ad-agencies at the same time.

The sell to clients was compelling.

Buy more media for the same $s and grow your business.

Buy the same media with less $s to invest in other things.

This approach won clients, grew trading pools and drove the relative price of media downwards.

In the pursuit of ever greater discounts, the deals some agencies were making to hit pricing commitments led to scenarios where planners were constructing plans and building arguments to get them signed off to service agency trading deals, more so than clients advertising and communications challenges.

Creating a gap in the market.

As it doesn’t matter how cheap your media is versus someone else’s if you’re buying the wrong thing.

Trading-Led Agencies meet Planning-Led Agencies

Smart media planners buddied up with savvy media buyers to launch agency propositions that emphasised the benefits of planning.

An approach my current employer was born from, pitting itself against “trading-led” shops that could help clients who knew what media they needed, access the cheapest inventory… with “planning-led” agencies figuring out what media would be most effective as well as how media may enhance creative work so it “sticks out” or is more memorable.

Then just as the dust was starting to settle…along came Google…and with it the internet at scale.

An initial experiment by Larry & Sergey to organise the world’s information, would go on to re-organise the advertising industry, becoming the largest advertising vendor in the world later down the line.

With that in-mind it for this post it would be crazy to go with anything other than

G is for…Google

Unlike some of my other posts I won’t break down the products and services they offer, and how to benefit from them at different points in the planning process, as there are plenty of materials online.

I thought it would be more interesting to focus on how they built the tools that gave them direct access to the CMOs and CEOs of the world’s largest advertisers.

Before focussing on the implications for media agency talent and agency operations, that have left us in an arguably stronger position than before they came along.

Where it all started…

At first glance sponsored listings, offered on a pay-per-click (PPC) basis, allowing businesses the chance to put their offering directly in front of people actively searching for associated products, services or understanding wouldn’t seem to be that much of a threat to media agencies – is because they didn’t offer that much of a threat to their existing business model.

The equivalence of PPC marketing “Pre-Google” would be direct mail or classified advertising, designed to trigger phone calls to call centres that could be counted and equated to sales and profit.

Personified by the classic Yellow Pages of yesteryear.

This was important for some types of clients but wasn’t where most agencies or publishers were making most of their money, or creating most value for the types of advertisers that were using their services.

Notably big advertisers, using broadcast media.

Google’s initial search product was valued enough by both users and clients, big and small, across sectors and geographies, that they generated more than enough cash to buy their way into dominant positions in other parts of the emerging digital marketing ecosystem.

Adding YouTube & DoubleClick to basket

Whilst Google’s acquisition of YouTube in 2006 made all the headlines, it was their acquisition of DoubleClick that has had more of an impact on agency operations today.

In 2007 Google was roughly a 10th of the size it is today but saw growth in the business where DoubleClick made its living.

To this point Google was giving away free software tools to help advertisers serve, track and optimise campaigns that DoubleClick had charged for.

To diversify and stave off the threat of Google eating its lunch, DoubleClick created a marketplace offering publishers the chance to sell excess inventory that their sales representatives couldn’t pre-sell to advertisers, electronically via an automated advertising auction/exchange, to ensure every impression they served to users ended up being monetised.

In doing so taking a % of each trade for themselves.

This move created a hugely valuable asset for DoubleClick… business relationships with thousands of publishers and ad-serving technology that could be scaled to millions more on both sides of the trade.

Offering the perfect ying… to Google’s yang …of its existing relationships with millions of search advertisers, big and small, resulting in Google having the most compelling bid in addition to the $3.1BN in stock they offered seeing them beat off competition from both Microsoft & Yahoo!

Alongside Doubleclick that was acquired in the desktop era, Google also bought start-ups that made software for publishers and advertisers within the emergent mobile ad ecosystem; including AdMob in 2009, Invite Media in 2010 and AdMeld in 2011.

Those building blocks being put together alongside its in-house innovations creating more spaces to sell ads (e.g. Mail, Maps etc) and more data signals from users (e.g. Chrome, Android, Mail, Maps etc) helped them create ever more targeted advertising, at increasingly higher yields, giving Google a dominant and lucrative presence in every step of the buying and selling of online ads.

They pieced it all together…the digital advertising market under one roof

Doing so before most media agencies had figured out WTF was going on with digital media and how to organise themselves to advise and execute for clients accordingly.

So how did this impact media agencies and media agency talent?

Practitioner wise this resulted in two noticeable shifts …

The further unbundling of agencies. A demand for “digital” talent.

The rise of digital advertising, split advertising budgets and responsibilities further and faster.

Instead of x-agency meetings having representation from client-side, creative, media & PR – suddenly there were digital client roles, digital creative agencies, digital media agencies and their subsequent splintering into search, social media and fast-forward to today with digital commerce equivalents.

Bigger meeting rooms. More voices. More agendas. More “strategies”.

Creating more demand for digital talent and the development of technical skills.

From Schedulers to Optimisers. A need for analytical skills.

With digital media being always on and always available, creating more lines of data to collate, count, distil and tinker with… resulted in reporting at a much higher frequency relative to its more traditional counterparts.

Changing the emphasis of agency talent from planning and scheduling media and the requirements to get it live, then get down the pub, to optimising activity towards the most favourable outcomes on an ongoing basis.

Depending on the nature of the client and how often they would like to look under the hood, this resulted in more and more time spent reporting media delivery and performance than planning it.

Creating more requirements for increasingly analytical skills.

The most profound shift happened outside of our day-to-day interactions with clients.

The Big De-positioning of Traditional Media & Media Agencies

Whilst The Yellow Pages online would have been of interest to some blue-chip advertisers, the market under one roof Google went on to create, gave an opportunity to have a much more expansive conversation with more senior decision makers than PPC advertising alone would have afforded them.

Once the door was open, they kicked straight through it, using a simple playbook that has been rolled out time and again, across different parts of its advertising product and subsequently martech stack – an approach that has been adopted by subsequent vendors and platforms that have come onto the scene.

My tongue is firmly in cheek, but you’ll be familiar with the below once you experience it in action…

- Ooh. We got a new thing to sell!

- Limit initial supply of new thing through “alphas” and “betas”

- Exclusivity of “alphas” and “betas” creates desire amongst marketers wishing to build their personal brand, who will appear in the broader industry marketing of the success of these alphas and betas

- Offer the best advertisers, that are the most widely known, who produce the best advertising, that’s the most likely to be effective, first refusal on those alphas and betas to prove-out the effectiveness of the new thing

- Unsurprisingly… hand selected alphas and betas prove successful for already successful advertisers, already successful advertising – be that to reach more people “vs. traditional advertising” or be more effective “vs. traditional advertising”

- Commission Big U.S. Consultancy that C-Suites of leading advertisers use to craft their business strategy, to create 2 waves of frameworks underpinned by the success of hand-selected alphas and betas, to credibly position the ways all advertisers must use new thing, or new combination of things to their advantage or risk being obsolete.

- First wave of frameworks… “Be authentic and cool, like our best users”

a la “Hero. Hub. Hygiene.” An early YouTube Content Framework

Or today’s equivalent “Don’t make ads make TikToks”

- Second wave of frameworks… “Be mature and effective, like our best advertisers”

a la “Bite. Snack. Meal.” More recent YouTube Content Framework

Or “Our most effective advertisers use a minimum of 4+ products, reaching a minimum of half the population” Facebook/META

- For both waves get in-house creative team to showcase how the most idolised brands make creative work that just so happens to fit the Big 4 Consultancy Model. Red Bull, Nike, Adidas or Burberry.

- Invite the most senior advertisers, with the largest wallets, the chance to enjoy this #content at Mountain View

- Create subsequent quarterly meetings with “viewfriends” where the vendor scorecards the brand and businesses’ adoption of the Big U.S. Consultancy Model

- Inevitably there is “room for improvement” which ensures CEO/CMO kicks marketing team, who kicks media agency or media department into closing the adoption (and investment) gap to make meetings less awkward for the most senior client moving forwards. Just get onto the wine please.

- In doing so more advertisers adopt more products, resulting in more revenue

- Repeat!

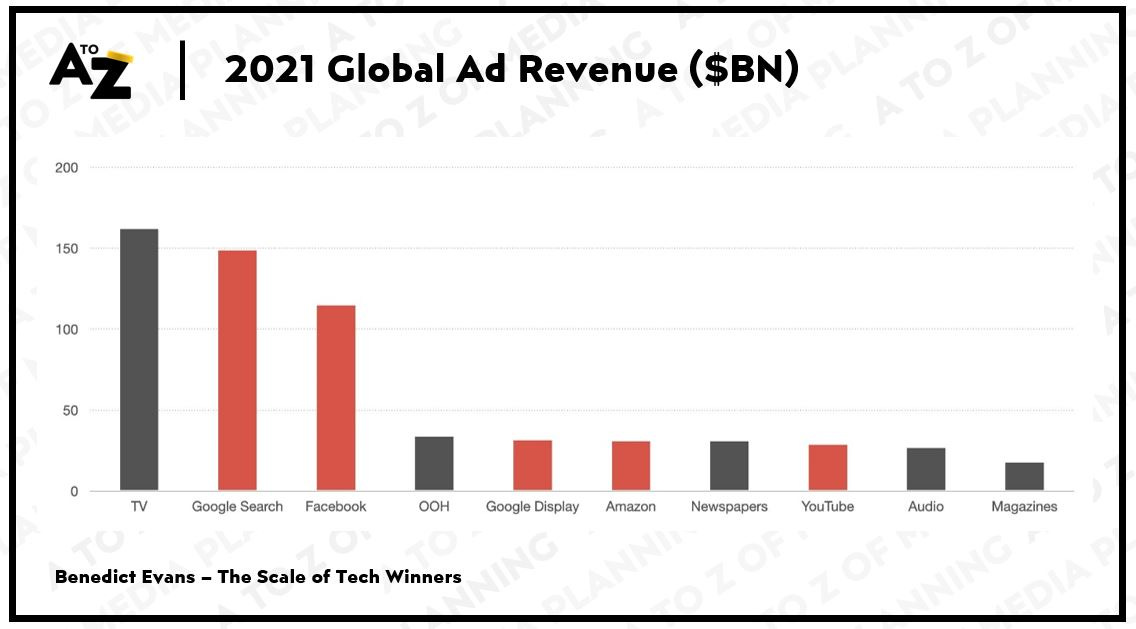

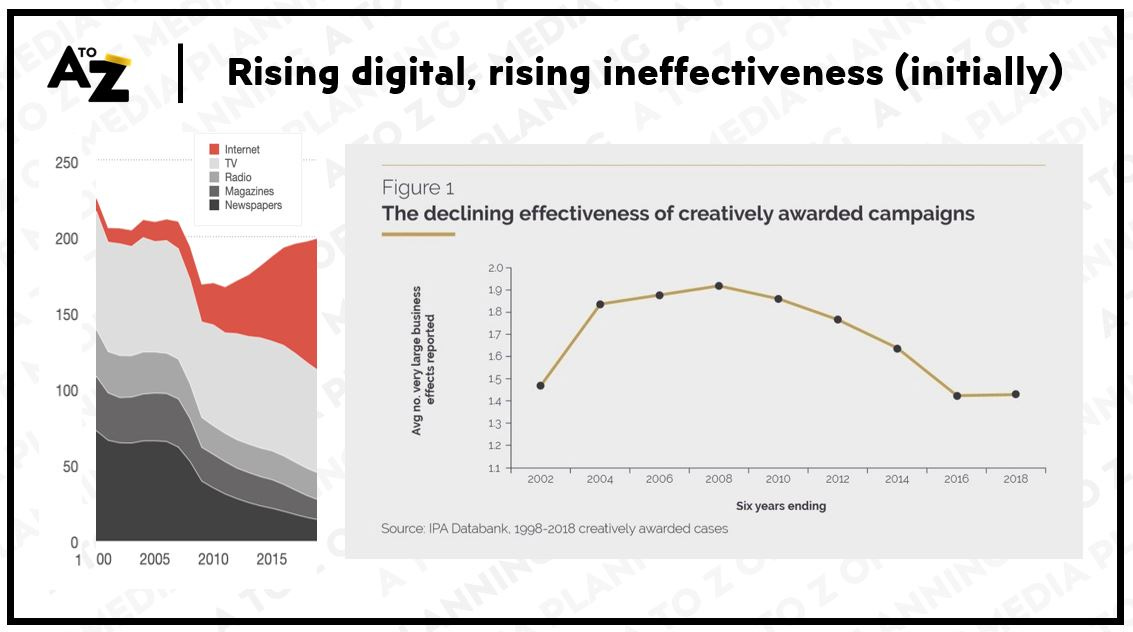

This approach has contributed to winning the hearts and wallets of advertisers big and small, with Google Search, Display & YouTube revenues surpassing Television advertising by value.

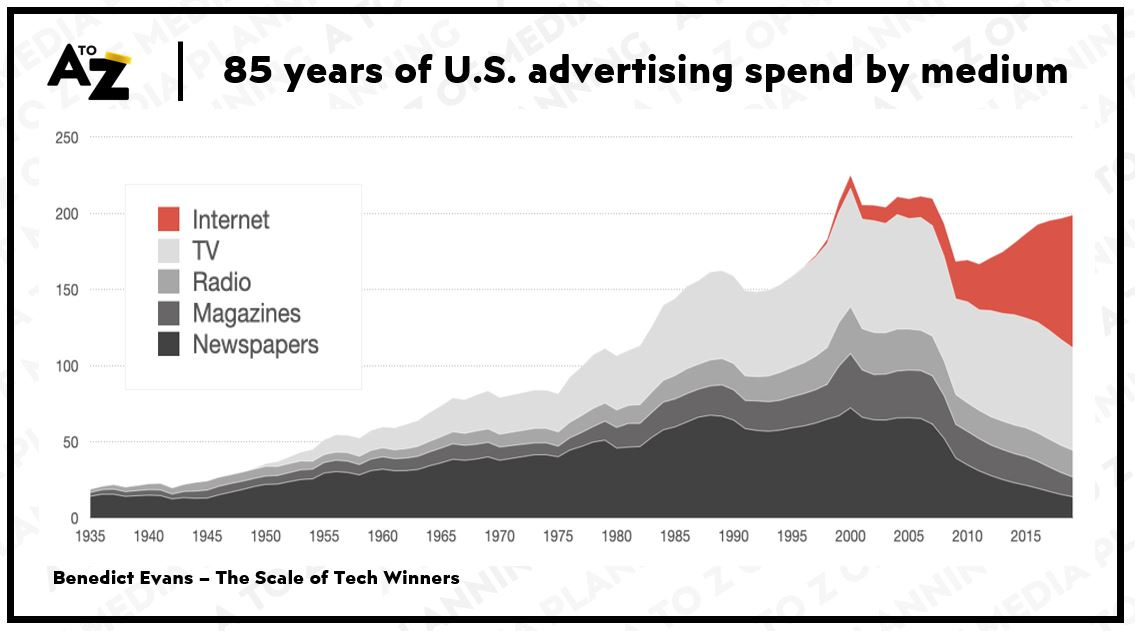

Resulting from a seismic shift of investment into digital channels, mainly to the detriment of newspapers…

…but does it work?

This shift in emphasis and investment also coincided with a rising ineffectiveness of advertising over time as much of the ideology being spun to sell digital marketing products and services, such as zeroing in on moments of truth, or targeting specific audiences otherwise unavailable in traditional media, didn’t end up translating into increased effectiveness as promised.

Like most things in life, balance is key.

Which is where good, open, honest and transparent partners and practitioners support clients in helping them to see the magic in what vendors new and old have to offer, but pull it apart from the bluster at the same time.

These flaws in the west-coast narrative and logic, created a new opportunity for media agencies and the talent within them to re-orient and re-position themselves in the client partner supply chain once again.

Media Departments -> Media Agencies -> Marcomms Orchestrators

Media agencies previously competed against other media agencies through their ability to plan insightfully and trade ferociously.

Whilst those requirements remain, media agencies have layered additional skills and services becoming increasingly responsible for…

- the majority of advertising investment and helping build cases for sufficient investment

- the construction and/or operation of the martech stacks that investment passes through

- the management of the associated consumer, campaign and creative performance data generated

- the integration across all campaigns, all channels and the associated tools and tech

- the extraction of relevant data as inputs from strategy <-> measurement and modelling

- the distillation of the above into implications across the above for adjacent agency and client disciplines

…amongst many other things - not just across one client or sector, but multiples of clients and sectors, elevating our discipline way beyond its original form.

Trading-Led -> Planning-Led -> Outcomes-Led

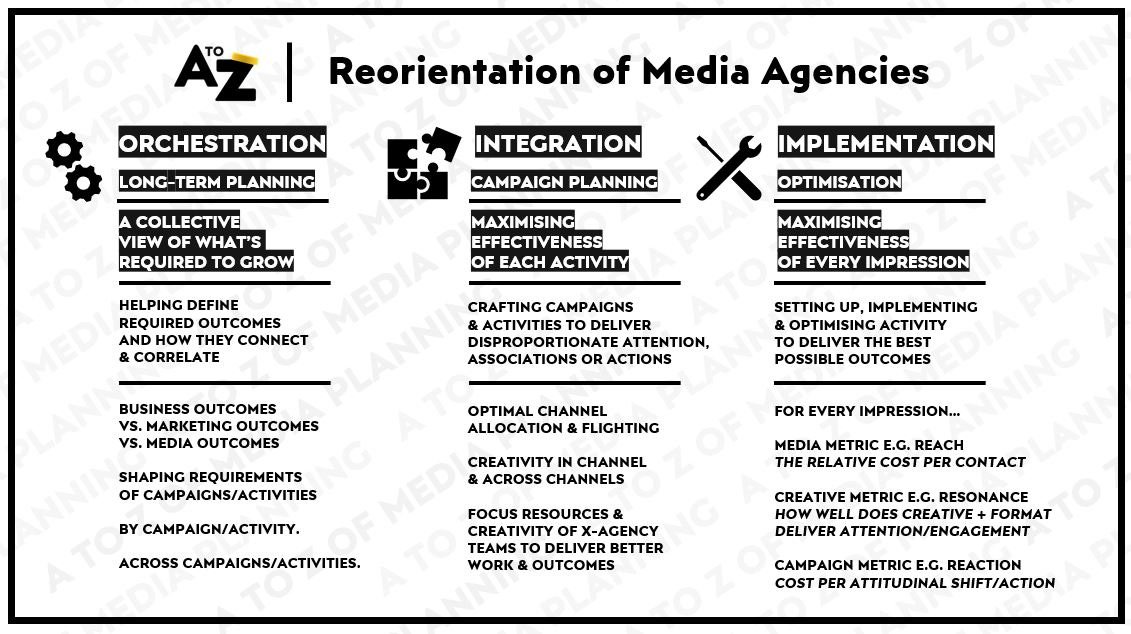

These additional responsibilities are seeing good media agencies and good talent within re-orient themselves from schedulers and co-ordinators and traders of advertising, into orchestrators.

Orchestrating longer term plans and tthe investment required to deliver them.

Integrating campaign plans across disciplines, whilst still retaining responsibility for the implementation, trading and optimisation of activity that’s happening today.

Some of which, not all of which is captured in the graphic below.

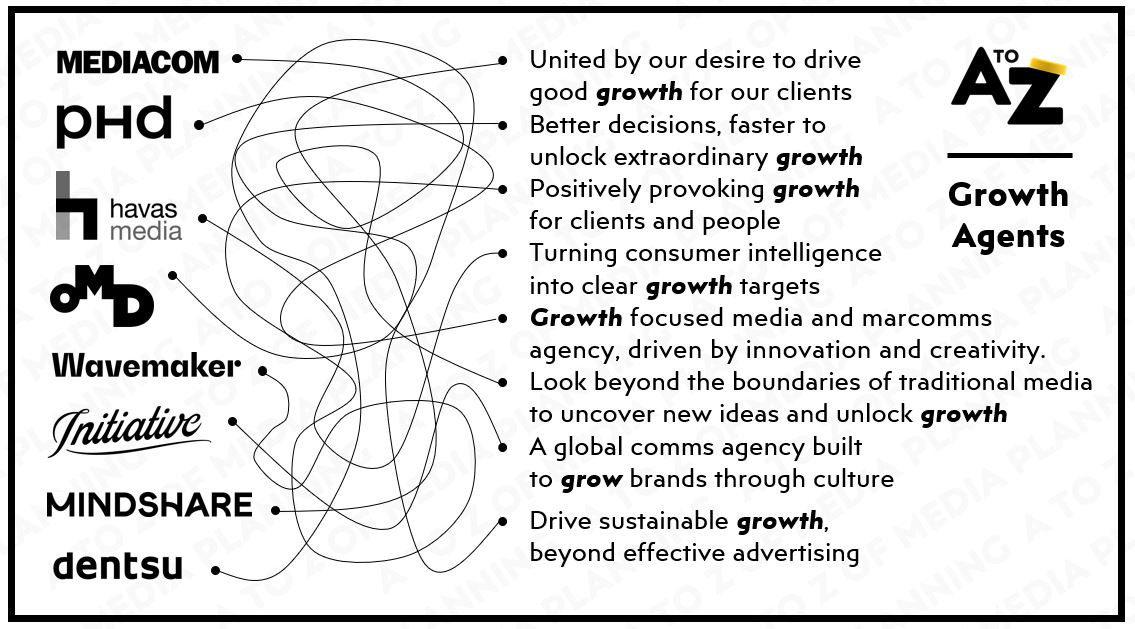

This broader responsibility, higher-up the x-agency chain of command has seen media agencies re-position themselves, from commoditised services that can be easily swapped in and out based upon the whims of a procurement team, to trusted advisors that become harder to detach from, well at least from good ones.

Hence why you’ll see most media agencies now positioning themselves as agents of growth, more so than agents of media as per the graphic below.

None of which would have been as possible, or probable without the digitisation of advertising and communications that Google themselves spearheaded – thus elevating the role of media and those with expertise with it.

So for that Google et al, we should thank you.

Until next time!